”The move from ‘clean’ to ‘clear’ labeling is a key trend for 2015, reflecting a move to clearer and simpler claims and packaging for maximum transparency,” says Lu Ann Williams, Innova’s director of innovation. “Meeting the needs of the Millennial consumer has also become a key focus, as has targeting the demands of the gourmet consumer at home, re-engineering the snacks market for today’s lifestyles and combating obesity with a focus on positive nutrition.”

Top food and beverage trends for 2015 are led by:

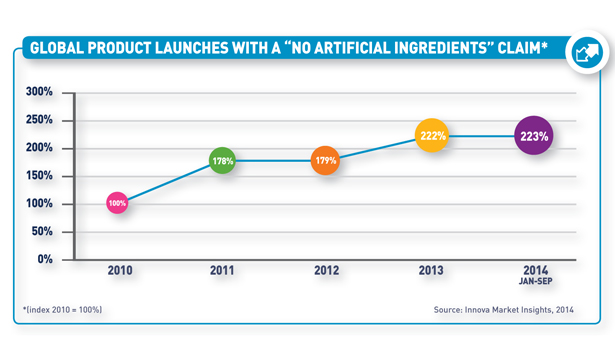

1. From Clean to Clear Label. Clean label claims are tracked on nearly a quarter of all food and beverage launches, with manufacturers increasingly highlighting the naturalness and origin of their products. With growing concerns over the lack of a definition of “natural,” however, there is a need for more clarity and specific details. Consumers, retailers, industry and regulators are all driving more transparency in labeling.

2. Convenience for Foodies. Continued interest in home cooking has been driven by cooking shows on TV and by blogging foodies. It is seen as fashionable, fun and social, as well as healthy and cost-effective. It has driven demand for a greater choice of fresh foods, ingredients for cooking from scratch and a wider use of recipe suggestions by manufacturers and retailers.

3. Marketing to Millennials. The so-called Millennial generation, generally aged between 15 and 35, now accounts for about one-third of the global population and is tech savvy and socially engaged. They are well informed, want to try something different and are generally less brand loyal than older consumers. They want to connect with products and brands and know the story behind them.

4. Snacks Rise to the Occasion. Formal mealtimes are continuing to decline in popularity and growing numbers of foods and drinks are now considered to be snacks. Quick healthy foods are tending to replace traditional meal occasions and more snacks are targeted at specific moments of consumption, with different demand influences at different times of day.

5. Good Fats, Good Carbs. With concerns over obesity there is a growing emphasis on unsaturated and natural fats and oils that has seen rising interest in omega 3 fatty acid content as well as the return of butter to favor as a natural, tasty alternative to artificial margarines that may be high in trans fats. In the same way, naturally-occurring sugar is being favored at the expense of added sugars and artificial sweeteners.

6. More in Store for Protein. The protein boom has been prevalent for years, starting off in the United States but currently impacting other regions in full force as well. Europe has seen an increase of 38% of total launches tracked with a protein claim, with cereals and dairy as key product categories. Protein is moving from the niches to the mainstream with mass appeal of such claims as satiety and everyday energy. From the supply side, sources of protein are proliferating with dairy proteins still growing strong, pea protein is showing great potential for the future and insect protein is the latest hype.

7. New Routes for Fruit. More product launches are being tracked with real fruit and vegetables, as consumers perceive a product to be healthier when it contains a real fruit or vegetable ingredient. Fruit and vegetable inclusions can contribute to the “permissible indulgence” character of a product. From an ingredient perspective, fruits and vegetable extracts can function as coloring foodstuffs. In that role, they can meet the increased demand for natural colors and flavors.

8. Fresh Look at Frozen. In order to compete with the healthy appeal of fresh aisles and the convenience of canned foods, established frozen foods (vegetables and seafood) are focusing on freshness in their marketing, stressing the superior nutritional content in frozen food. Brand extensions include wider varieties of vegetables and fruits. At the same time the frozen segment is witnessing new product launch activity in new categories (e.g. soups, fruit, drinks, finger foods, sauces, pastries, herbs).

9. Private Label Powers On. Private label (PL) brands are here to stay and are even growing in terms of category offerings. Once mostly found in staple goods, PL is now observed on shelves where brand equity and loyalty among consumers is the highest, e.g. chocolate and personal care. This indicates that PL quality is not only improving, but consumer perception of PL quality is increasing accordingly. Discounters are no longer solely seen as budget stores by consumers, but are gaining acceptance and are considered to have good quality products. Their fresh produce aisles have stepped-up considerably in quality as hard discounts are increasingly being seen as one-stop-shops by consumers.

10. Rich, Chewy & Crunchy. Texture is an important driver for taste perception for food and beverages and is the focus of many of today’s food innovations. Brands are creatively combining textures with for example crispy inclusions, soft centers and extra crunchy toppings. Texture claims are shown more prominently on front-of-pack. Also, brands are creative in describing texture or including a texture claim in a product name.

Innova Market Insights is a global provider of market intelligence and insights that drives innovation in the food and beverage industry. The Innova Database (http://www.innovadatabase.com) is the product of choice for the whole product development team. Track trends, competitors, ingredients and flavors.

Gluten-Free Still Growing

It seems these days, grocery shelves are exploding with gluten-free choices, due in large part to greater awareness of a gluten-free diet as a result of increasing diagnoses of celiac disease and other gluten sensitivities, and the diet’s perceived health benefits. So it’s no surprise that recent Mintel research finds the gluten-free food market is estimated to reach sales of $8.8 billion in 2014, representing an increase of 63% from 2012-14.

“Overall, the gluten-free food market continues to thrive off those who must maintain a gluten-free diet for medical reasons, as well as those who perceive gluten-free foods to be healthier or more natural,” says Amanda Topper, food analyst at Mintel. “The category will continue to grow in the near term, especially as FDA regulations make it easier for consumers to purchase gluten-free products and trust the manufacturers who make them. Despite strong growth over the last few years, there is still innovation opportunity, especially in food segments that typically contain gluten.”

All gluten-free food segments increased in the past year, though the snacks segment increased the most. Gluten-free snacks increased 163% from 2012-14, reaching sales of $2.8 billion. Sales increases were mainly due to a 456% increase in potato chip sales. Meanwhile, the meats/meat alternatives segment is the second-largest gluten-free food segment in terms of sales, reaching $1.6 billion in 2014, a 14% increase from 2012-14. What’s more, the bread products and cereals segment saw gains of 43% during that same time period, and is set to reach $1.3 billion this year. Bread and cereal are ripe for gluten-free growth with only 1% of the overall segment termed gluten-free.

“Gluten-free products appeal to a wide audience; 41% of US adults agree they are beneficial for everyone, not only those with a gluten allergy, intolerance, or sensitivity. In response, food manufacturers offering either gluten-free alternatives or existing products with a gluten-free label have increased dramatically over the last several years,” adds Topper.

But it seems not everyone is convinced of gluten’s health attributes. While 33% of survey respondents in 2013 agreed that “gluten-free diets are a fad,” the number increased to 44% of Americans in 2014. However, that hasn’t slowed gluten free’s popularity—22% of Americans currently follow a gluten-free diet, compared to 15% in 2013.