NEW PRODUCTS:NORTH AMERICA: A Moveable Feast

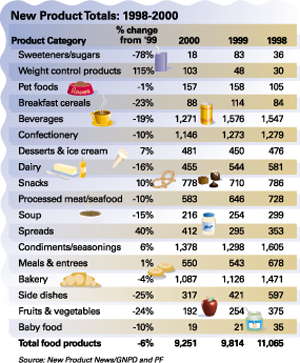

Although new food and beverages exhibited innovation, the number of product introductions in 2000 was down about 6% compared to the year before. This continues the pattern of decreasing new product introductions for the past several years. The difference between this last year and the previous, however, was smaller than it has been between year-end totals over the past few years, which may mean that the downward spiral is leveling off.

Top 20 Bulk Up

While the total number of food and beverage products was essentially flat in 2000, the number of introductions from the 20 most product-prolific food and beverage companies increased due to consolidation. Who would have thought when we did our Top 20 ranking for 1999 that six of the companies on that list would be acquired by others, four of which also were on that Top 20 list?For the Top 20 Food Company ranking in 2000, Philip Morris topped the list, but probably because Kraft acquired Nabisco. General Mills came in second, mainly due to its acquisition of Pillsbury. Unilever was No. 4, driven by its takeover of Bestfoods (part of which it has since sold off). PepsiCo made it onto the list with its South Beach Beverage (SoBe) and Quaker buys. Kellogg rose in the rankings, helped by both the Keebler and Morningstar Farms acquisitions. Cadbury made it on the list for the first time because of Triarc Beverages (Snapple).

Given the acquisition fever, it also comes as no surprise that several companies made the list that normally don't, or don't very often. New Organics Company, new to the list and Prepared Foods' 2001 New Products Company of the Year (see article beginning on p. 8) offered a broad 50-item line in 2000, all organic and mostly sold in health food stores.

Crabtree and Evelyn was new last year as well, with jams, sauces and other gourmet delicacies. Both Frieda's and World Variety Produce occasionally make the list; both did this year with new vegetable varieties. Although Aurora Foods has had its troubles, it managed to introduce more products in 2000 than in 1999, boding well for its investors. M&M/Mars seems to make our ranking every other year or so; it found a place in 2000 because of its Seeds of Change organic sauce line.

Several other companies that usually are on the list did not fare as well in 2000 as they had in prior years. Hormel squeaked in at No. 20, with a significant downturn in the number of introductions. Hormel seemed to focus more on its mainstream lines (i.e., Spam) rather than its gourmet food products. Although Dreyer's continued to offer new ice cream varieties, it did not top 1999's record for the company.

Lowfat Makes a Comeback

The big changes in 2000 weren't just in the number of products introduced by the biggest companies. Also of note were new products bearing particular nutrition claims.Most significant is the activity with lowfat product introductions. It appears that 1999 may have been just a blip on the lowfat barometer. After a year that saw only 481 new products in that category, 2000 came on strong with 1,057 introductions. That's still down quite a bit from the 1996 high of 1,914, but represents a major uptick from '99.

One of the major categories in which lowfat foods showed up was in milk and milk substitutes. Many of the products in this active subcategory are not made from milk, they're made from soy. Those products, almost exclusively, promote themselves as being lowfat or fat-free.

Of course, the Meals category contained a number of lowfat entries, as did Processed Meat. In the latter category, however, the big news was meat substitutes. Again, credit soy, which appeared in a variety of forms. Soy also had an impact in the Snack Bars subcategory, as energy bars of all types and varieties promoted their soy content and their lack of fat.

Surprising to us was the low number of reduced-calorie food introductions. Now, it must be remembered that the products we count in each of these claims are ones that actively promote the claim. Therefore, if a product is low calorie but does not promote itself as such (in trade literature or on the package itself), it is not categorized as being low in calories. Perhaps, more products are relying on the consumers' understanding of the Nutrition Facts panel on the back of the box.

The same could be said with the low sugar claim. We had anticipated seeing more products flagged as being low in sugar, with the growing incidence of diabetes. However, Nabisco did extend its line of SnackWell's cookies with sugar-free varieties. The biscuit king removed the sugar but added fat to these new flavors, which are no longer touted as lowfat.

Naturally Good-for-You

The group of claims showing the most growth last year promoted the essential "goodness" or wholesomeness of a product. Those claims--all natural, no additives/preservatives, and organic--have enjoyed steady growth in the last few years. Although the no additives/preservatives total was down in 2000 from 1999, it still represents a significant increase from the late 1990s figures.Organic products continue to hit the marketplace, with 844 introductions last year. Aside from organic coffees and teas, the organic product introductions seem quite evenly distributed among the product categories, with significant entries appearing in both grain-based categories (bakery, cereal, snacks) and meat-based ones (meals, processed meat). The vagaries of the U.S. economy may have a detrimental impact on organic introductions in the future. Expect fewer organic totals this time next year.

The two categories of claims that focus on what's added into products also showed gains last year. Added-calcium products reached an all-time high, while the added-fiber product total was the highest it has been for almost a decade. Watch for calcium-enriched products to continue to increase as Baby Boomers grow older and discover the needs of additional calcium in their diets. The added-fiber growth is also probably due to the Boomer influence. PF

Nutrition Facts

| Products Bearing Nutritional Claims, 1998-2000 | % change | ||||||

| Product Category | from '99 | 2000 | 1999 | 1998 | |||

| Reduced/low calorie | -14% | 261 | 302 | 456 | |||

| Reduced/lowfat | 119% | 1,057 | 481 | 1,180 | |||

| All natural | 116% | 1,130 | 522 | 743 | |||

| Reduced/low sodium | 35% | 131 | 97 | 80 | |||

| No additives/preservatives | -23% | 269 | 346 | 149 | |||

| Low/no cholesterol | -23% | 189 | 244 | 124 | |||

| Added/high fiber | 20% | 81 | 67 | 43 | |||

| Reduced/low sugar | -18% | 61 | 74 | 164 | |||

| Added/high calcium | 32% | 158 | 119 | 45 | |||

| Organic | 7% | 844 | 783 | 842 | |||

NOTE: Nutritional claims categories are not cumulative, as new products may carry more than one claim.

Source: New Product News/GNPD/PF

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!