The Future of Physiologically Beneficial Foods

|

Although the functional product sales have and will continue to rise at a faster rate than the global food and drinks industry as a whole, growth in parts of the global functional foods market appears to be slowing, due mainly to economic reasons. Many functional foods are priced at the upper end of the market. Other factors include a slight maturing of certain sectors, consumer fatigue and the fact that various authorities have started to impose limits upon the health claims made by such food and drinks, Leatherhead notes. “Nevertheless, levels of new product activity remain reasonably high, and health trends observed throughout the developed world (such as rising obesity rates) suggest that the market potential for many types of functional foods remains positive.”

The report uses the strict market definition of functional foods as “everyday” food and drink products (not pills, supplements or portions) that bear a specific health or physiological claim implying the product has an effect over and above that of just nutrition (e.g., helps lower cholesterol as part of a low-fat diet, helps maintain a healthy heart, improves the body’s natural defenses, enhances performance or boosts energy level, etc.). The report also considers products with healthy or functional positionings, such as products fortified with calcium, minerals and antioxidants, whose content/use is highlighted but may not feature health claims.

Where the Value Is

The Leatherhead Food Research report says the international functional food and drink market (defined as products making a specific health claim and not including energy and mood-enhancing foods and beverages) was worth some $24.22 billion in 2010, with an expected growth of 4-5% in the next few years. By 2014, the international functional foods market is forecast to have a value of some $29.75 billion.

With a value share over 38%, Japan is currently the largest market for functional foods. However, Japan’s FOSHU (Foods for Specific Health Use) includes not only foods with health claims but, also, those with purported medicinal benefits, such as herbal remedies; because of this, a direct comparison is difficult. The U.S. follows Japan with 31.1% of the global market (up some 31% compared to 2006), and Europe comes in third place with 28.9% of the market. It has been noted estimates for the size of the U.S. functional foods market vary according to the definitions used.

Although all regions should have significant gains, the report sees the U.S. and European markets as driving growth, since there are still some relatively undeveloped sectors compared to the more mature Japanese market. Also, it notes some of the recent global growth in functional foods is appearing in less developed markets, such as China, India, Latin America and Southeast Asia.

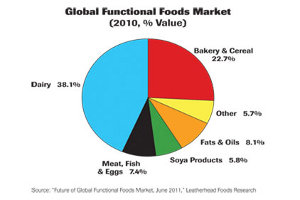

If the strict definition of functional foods is used, the global functional foods market is dominated by dairy products, with sales valued at $9.23 billion in 2010, equivalent to more than 38% of the overall industry. Although it continues to hold a strong position in Europe, functional dairy products are also making much headway in the U.S., owing to the success of probiotic yogurt drinks. Given the fact that the Actimel and Activia brands now account for about a quarter of market leader Danone’s annual revenue, the dairy sector is expected to retain its dominant position for some years to come.

The bakery and cereal product sector accounts for almost 23% of the world’s functional foods market and has been one of the best performers since 2006, having expanded in value by more than 54%. The Leatherhead Food Research report notes much of the growth has been due to the increasing number of cereal-based products being marketed on a heart-health platform, particularly in the U.S. A large number of products are being marketed on a specific health platform, such as whole grains or oat content, allowing them to use FDA-approved health claims.

The report notes energy/mood enhancement, gut health and heart health are the dominant sectors for claims being made, although there has been fairly strong growth in weight control and immunity. Bone health and anti-aging claims have been relatively rare in foods, but far more popular in dietary supplements.

It is estimated product failure rate within the global functional foods market may be as high as 80%. Besides consumer skepticism over the efficacy of functional health claims, such foods are less likely to succeed, if they are perceived to lack taste and flavor.

There are several factors important to future growth. For one, “health claim regulations in Europe are currently under scrutiny, and the future of other global regulations will shape the health claims permitted on packaging.” As regulations are likely to become stricter, only health claims with strong scientific backing will be permitted for use or would be endorsed. The communication of the science underpinning functional foods is important.

Consumers are also becoming savvier to the concept of “scientifically proven” and what it means. They are also skeptical. Clarity of the products’ positioning and communicating product benefits to consumers will be crucial. pf

|

Facts and Figures |

|

* In the U.S., coronary heart disease is currently responsible for 97.6 deaths per 100,000 people. This compares with 90.1 for the UK, 89.7 for Germany and 72.8 in Australia. * All regions saw significant growth in demand for functional foods between 2006-2010, with Japan’s FOSHU market having risen by 46.6% during this time. At more than 39%, growth within the Australian market has also been on the high side. * Some 26% of U.K. people claim to consume functional food and drinks on a daily basis, a figure which decreases to 20% for those claiming to consume them on a weekly basis. However, 30% claim never to buy into the category at all. |

This article was drawn from “Future Directions for the Global Functional Foods Market,” June 2011, by Leatherhead Food Research. The report reviews sales of functional foods in the world’s key markets, in areas such as anti-aging and heart, gut and bone health. It also explores consumer attitudes, recent regulatory developments, industry structure and trends in new product activity. An analysis of consumer attitudes towards functional foods and beverage; the industry’s major players and their brands; a review of recent new product activity; and a discussion of future strategic directions are also featured. For more information: publications@leatherheadfood.com, www.leatherheadfood.com/functional-foods, +44 (0)1372 822376.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!