Foodservice Operators Strive for More

Positive gains in the restaurant industry can be attributed to those chains providing a “better” experience.

Last year, Starbucks overtook Subway for the number-two spot in the Top 500. This year, Starbucks continued its growth, leading the way for top chain sales and unit growth with $13.9 billion in US sales and 13,066 US units.

Chicken restaurants are popular within LSR segment—led by Chick-fil-A.

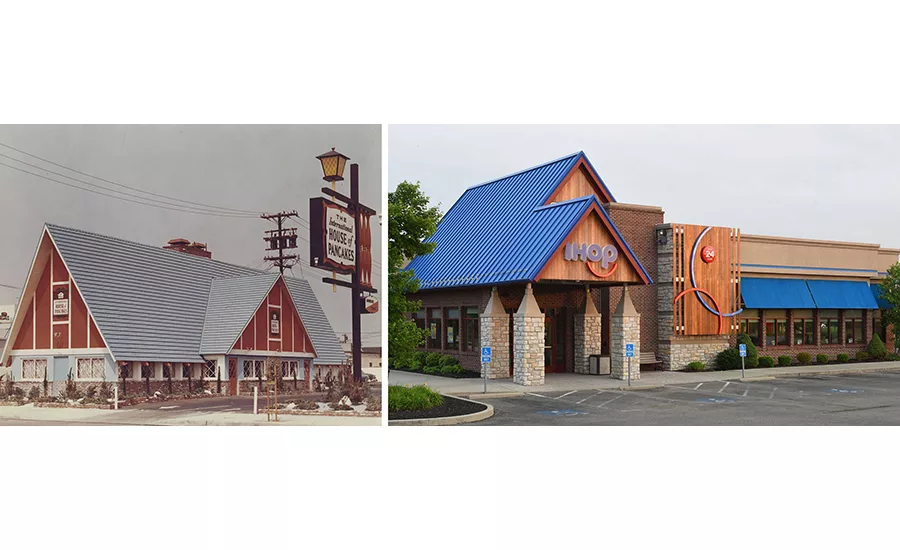

IHOP started in 1958 in Toluca Lake, Calif. The popular chain celebrated its 58th anniversary this summer with 58-cent pancakes.

McDonald’s announcement that it would offer its popular breakfast menu all dayproved to be a winner among McDonald’s customer base.

Increased consumer optimism and an improving economy proved positive for the restaurant industry as it ushered in a year of growth in 2015. Leading restaurant chains ranked by sales fared even better than the industry overall, particularly in unit growth. Despite an influx of competition, restaurants appear to be on a growth trajectory, carving out their own niches to capture varying consumer occasions.

Industry-wide sales approached $500 billion, topping out at $490.8 billion for the year—an increase of 4.8% from 2014. Unit growth held steady at 1.2% over the previous year.

More than half of the restaurant industry’s sales in 2015 came from the sales of Technomic’s Top 500 restaurant chains ranked by US sales, totaling $287.6 billion. Growth within the Top 500 reveals an uptick in same-store-sales in 2015, with a year-over-year increase of 5% in sales and 2.1% growth in units. Much of the growth in both sales and units occurred in the limited-service area of the Top 500 listings.

Limited Service

Roughly three-quarters of the Top 500 restaurant chains in 2015 were limited-service restaurants (LSRs), responsible for a 5.5% growth in sales to total $211.4 billion. The segment expanded units at a rate of 2.3%, to drive the 2.1% rise in total unit growth for all segments in the Top 500.

The menu categories leading the charge were Asian/Noodle, led by Panda Express (which saw sales increase 11.9%); Coffee Cafe, led by Starbucks (sales up 12.8%); and Chicken, led by Chick-fil-A (sales up 8.8%). Last year, Starbucks overtook Subway for the number-two spot in the Top 500; this year the chain continued its growth, leading the way for top chain sales and unit growth with $13.9 billion in US sales and 13,066 US units. Other top chains in sales growth were Taco Bell, with total US sales of $9.1 billion; and Domino’s, with total US sales of $4.7 billion.

Fast-casual’s grip on the LSR segment held steady in 2015. These concepts comprise about 16% of sales and nearly 13% of units for the limited-service industry, up from 15 and 12%, respectively, in 2014. Unit performance is where fast-casual shines; even though these restaurants make up less than one-fifth of sales, they boasted an 11.5% growth rate in sales in 2015 and a 9.6% rate of unit growth year-over-year. The sub-segment’s continued growth shows consumers are still “trading up” for a better value via low-cost, convenient meals with better-for-you ingredients.

“Better” everything is in high demand. Restaurants are repositioning and revamping their brand story around a prevailing theme of “better”—not only to stand out, but also to highlight freshness and quality.

Impressive growth at Jimmy John’s Gourmet Sandwiches (up 17.2% in sales, 16% in units) and Jersey Mike’s Subs (up 28.6% in sales and 22.1% in units) in the area of better sandwiches contrasts the struggling performance of Subway. The third-largest chain, ranked by US sales, saw its sales fall by more than 3% for the second consecutive year.

“Better” food fast proved to be its own niche for growth, as QSRplus chains have carved out space between fast food and fast casual with fresher menus, elevated service models and build-your-own formats. These QSRplus brands, like Culver’s, In-N-Out Burger, Pita Pit, El Pollo Loco and Chick-fil-A, have successfully molded this distinct category to take on fast casual and make gains in 2015.

A brand story around the “better” theme should include a narrative that highlights transparency to assure patrons of where food comes from; how it’s made; and what it contains. Consumers’ increasing demand for transparency will require more chains to communicate sourcing, ingredients and preparation methods for its food, revealing a shift in how brands market themselves and tell their story.

Not only does transparency provide a brand narrative, it also connects with a human, emotional component that is centered on social responsibility, sustainability, food safety and animal welfare. This narrative is most attractive to Millennial and Gen Z consumers—frequent foodservice users—who are likely to place more value on brands that align with their personal values and support causes they care about, according to Technomic consumer data.

This can both help and hurt chains, illustrated by missteps on the part of Chipotle, which for years has reaped the benefits of its position as among the original set of fast casuals. The chain built trust among consumers for its better-for-you positioning that includes responsible sourcing practices and use of natural, non-GMO ingredients. Its stock prices have taken a hit in recent months, following concerns over food safety and a federal inquiry after hundreds of people fell ill from eating at different Chipotle restaurant locations. Same-store-sales in the fourth quarter of 2015 were down 14.6%. Customers so far appear unmoved by Chipotle’s management of the crisis—which included temporarily closing sites, rolling out deep discounts and mandating food safety training for employees—as same-store sales continued to drop by almost 30% in the first quarter of this year.

Among this year’s other major industry headlines was McDonald’s announcement that it would offer its popular breakfast menu all day, a strategy that proved a winner among McDonald’s customer base. In 2014, the burger behemoth’s US sales were down 1.1%; although its unit growth declined by 0.6%, its sales in 2015 rebounded for a 1.1% increase.

The move to all-day breakfast not only opened up a new growth channel to reverse declining sales for the country’s top chain by sales—it also spurred growth among its competitors, who quickly began expanding breakfast offerings and extending breakfast hours. It’s likely that more LSR chains will continue to build on the momentum of all-day breakfast via signature sandwiches and other handhelds, as well as new value bundles.

Full Service

In the full-service segment, 2015 looked much like 2014. Full-service chains in the Top 500 saw a 3.6% increase in sales, the same as it had in 2014, for a total of $76.3 billion. The number of FSR units remained steady, rising 0.8% to about 28,400 units. Steak and Family Style menu categories are responsible for much of the growth in the segment. Sales at Steak concepts were up 6%, led by Texas Roadhouse (sales up 13.2%); and at Family Style chains, sales grew 3.1%, led by IHOP (sales up 8.1%). As in 2014, the fine-dining sub-segment saw the most growth in sales at 5.9%, followed by casual dining (up 3.5%) and midscale restaurants (3.2%).

High-end FSRs—including fine-dining and upscale and contemporary casual-dining concepts—are the fast casuals of the full-service segment. These chains have honed the “better,” elevated dining experience toward which more consumers are gravitating. Their continued focus has paid off, as some of these chains were ranked as some of the fastest growing concepts, including Seasons 52 (sales up 13.5%), Fogo de Chao (up 11.7%) and Yard House (up 11.2%).

One new entrant into the Top 500 highlights how full-service restaurants can succeed by refining their focus to one area—much like fast casual’s narrow, yet high-quality menus. Casual-dining chain The Boiling Crab offers a more laid-back experience than traditional seafood concepts, which have struggled in recent years because of their high price points. As in 2014, many of the major FSR seafood players saw their sales decline in 2015: Red Lobster’s sales were down 0.6%; Joe’s Crab Shack, down 4.3%; and McCormick & Schmick’s, down 6%.

The Boiling Crab’s simple menu lists seafood by the pound in a choice of Cajun-style seasoning and sauce. Restaurants offer no silverware or plates—servers provide bags of seafood boils on paper-topped tables for diners to dive into with their hands (no doubt a part of the ambiance and experience of a seafood boil, but also a way to keep costs down). Restaurants are known to have wait times of at least an hour during peak dining periods, a testament to the attractiveness of the carefree setting and flavorful fare.

The Boiling Crab, with its 17.2% year-over-year growth in sales and 6.7% increase in units, could be the answer to improving the sluggish full-service seafood segment. Inspired by The Boiling Crab’s popularity, a number of seafood boil concepts have launched in major markets across the US in the last year or so, as customers seek a new take on seafood restaurants.

Forecasting for the Future

In 2015, clean eating was equivalent to healthy in the eyes of consumers. Consumers’ preferences have shifted toward more real ingredients when they dine out, which led major chains, like Panera Bread and Pizza Hut, to remove additives from their menus in 2015. As more top chains respond to these shifting consumer demands, suppliers, too, will need to modernize to bridge the gap.

Additionally, technology’s role in the customer experience will continue to expand; interconnected, simplified technology that offers a seamless, efficient experience for restaurant patrons is becoming a must-have. Several top full-service chains—including Red Robin, Texas Roadhouse and Olive Garden—are catering to convenience-seeking patrons by adding on-demand amenities, like tabletop tablets, delivery service and mobile payment.

Limited-service concepts have really been at the forefront of using technology like reward programs, mobile ordering, and payment and delivery to attract and retain customers. The ability of predictive-analytics to trace customer preferences and spending can reward loyalty among guests and also create growth opportunities for leading restaurant chains and suppliers to collaborate on product development.

Beyond customer-facing options, technology that cost-effectively aids restaurant chains in labor management and scheduling is helping to mitigate labor costs in markets where wages are rising. It will be crucial that restaurants take advantage of technology as a cost-cutting tool in the face of rising labor and food costs, especially as consumers, particularly younger ones, continue to support minimum wage increases.

Originally appeared in the August, 2016 issue of Prepared Foods as Operators Strive for More.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!