Online Grocery Pickup Sales Defy Broad Downward Sales Trend

Ship-to-Home drove vast majority of the 8% drop in total sales while delivery also contracted

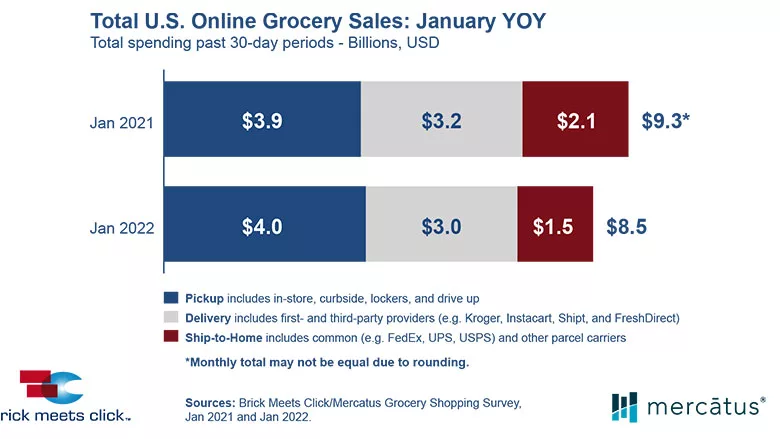

The US online grocery market generated $8.5 billion in sales and accounted for nearly 12% of total grocery spending during January, according to the Brick Meets Click/Mercatus Grocery Shopping Survey fielded January 29-30, 2022.

Total January sales were down 8% versus the prior year with mixed results across the three receiving methods (Pickup, Delivery, and Ship-to-Home). Only Pickup made sales gains, growing almost 2% to $4.0 billion. Delivery contracted 7% to $3.0 billion and Ship-to-Home sales plummeted 30% to $1.5 billion, driving nearly two-thirds of the total YOY sales decline.

“These sales results show that circumstances connected to COVID continue to disrupt the way people shop, but in different ways than earlier in the pandemic,” said David Bishop, partner at Brick Meets Click. “Increases in COVID case rates no longer have the same effect on buying patterns due in part to progress with vaccinations. The loss of financial assistance is another factor since the economic impact payments and child tax credits that many households received in 2021 have ceased. And, if that’s not enough, many retailers altered store operations in January to address the labor shortages associated with COVID-related absences and a tighter labor market.”

In terms of market share for January 2022 versus year ago, Pickup’s share of online grocery sales grew nearly five percentage points to 47% due to gains in its monthly active user (MAU) base and order frequency, and Delivery’s share grew just under one point to 35% due to increases in order frequency and spending per transaction. In contrast, Ship-to-Home’s share of online sales fell over five points from January 2021 to 18%, setting a record low that is more than 20 points lower than pre-COVID levels (August 2019).

The number of US households that bought groceries online during the month remained relatively steady at 69.0 million, dipping just 1% versus last year. Even so, the way in which households receive online grocery orders continues to evolve. For instance, the number of MAUs receiving an online grocery order via Pickup grew 6% while Delivery decreased by 2%, and Ship-to-Home fell by 8% year-over-year at the national level.

January finished with an average of 2.7 orders per month placed by MAUs, 5% fewer than January 2021 but still 33% higher than pre-COVID levels (August 2019). The year-over-year drop was entirely due to a pull-back in Ship-to-Home’s order frequency, which contracted by 36% while Pickup and Delivery expanded by 26% and 10% respectively.

The weighted average order value (AOV) across all three receiving methods in January 2022 remained essentially flat, declining less than 0.5% versus one year ago, but the results for each receiving method varied. Spending on Ship-to-Home orders shrank the fastest during the period as its AOV dropped almost 11% compared to a 3% reduction for Pickup and a 2% gain for Delivery.

For cross-channel shopping, the share of Grocery’s MAU base that also shopped online with Mass during the month pulled back two percentage points from a year ago and finished at more than 26% for January. The likelihood for an online grocery shopper to use the same service again within the next month jumped almost four percentage points on a year-over-year basis, coming in at 61% for January 2022. And, while that’s a positive trend, Grocery trailed Mass by seven points, giving up most of the gains it experienced in December as its repeat intent rate dipped back down to 58%.

“Grocers have a clear opportunity to drive stronger repeat purchase behavior,” said Sylvain Perrier, president and CEO, Mercatus. “In addition to providing a great customer experience, they also need to understand which loyalty drivers are unique to their customers and brand. When it comes to online grocery shopping, consider adding perks that cater to behavioral and emotional triggers, like offering a wider range of preferred pickup times or more frequent pickup time slots.”

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!