US eGrocery Sales Total $8.7 Billion in March

Q1 results finished less than 3% lower than a year ago as eGrocery continues to evolve

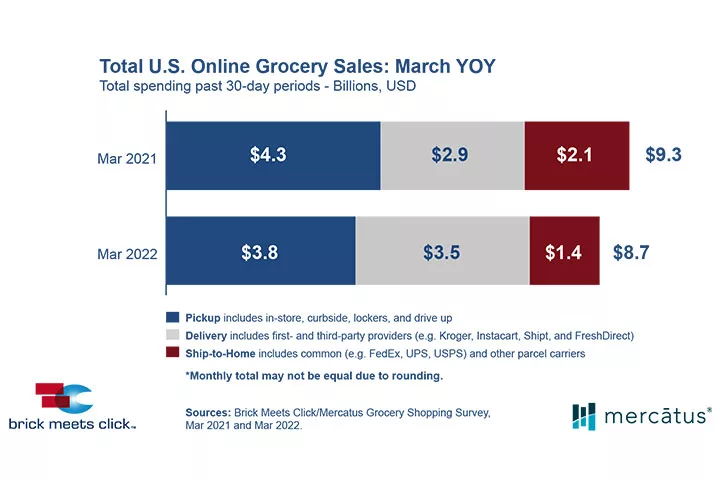

In March, total US online grocery sales pulled back 6% to $8.7 billion versus March 2021’s record high of $9.3 billion, according to the Brick Meets Click/Mercatus Grocery Shopping Survey fielded March 28-29, 2022. Total sales for 1Q 2022 ($8.5B in January and $8.7B for both February and March) finished just 2.5% lower compared to a year ago.

March YOY performance across the three eGrocery segments varied as the online grocery market continues to evolve.

The Ship-to-Home segment experienced the largest sales contraction, plummeting over 30% in March compared to a year ago, from $2.1 billion to $1.4 billion. The decline was driven by a 13% reduction in the number of orders placed by Monthly Active Users (MAUs) combined with a 23% drop in the average order value (AOV).

Pickup sales declined almost 11% in March from $4.3 billion in 2021 to $3.8 billion in 2022, affected by similar factors but to different degrees. Order frequency for Pickup declined 8% while AOV dipped less than 4% versus the prior year.

In contrast, Delivery reported strong sales growth for March, surging over 20% on a year-over-year basis from $2.9 billion to $3.5 billion. The number of orders placed by MAUs climbed by 13% and AOV rose 7% versus 2021.

Cross-shopping between Grocery and Mass gained momentum as the share of Grocery’s MAU base that also shopped online with Mass during the month increased nearly 4%age points versus last year, finishing at 29% for March 2022.

The likelihood for an online grocery shopper to use the same service again within the next month also increased during March, climbing to almost 64%, up 1.4%age points on a year-over-year basis. Analyzing month-over-month results showed that March repeat intent rates at Mass providers improved 8 points while Grocery’s intent rates lost more than 5%age points versus February 2022.

On a quarterly basis, total eGrocery sales for Q1 2022 were just 2.5% lower versus Q1 2021, with Ship-to-Home down 29%, Pickup down 2%, and Delivery up 15%. Ship-to-Home ceded 6 points of market share to Delivery while Pickup, the dominant segment, held steady. During the first quarter of 2022, Ship-to-Home finished with 17% of eGrocery sales while Pickup’s share remained essentially unchanged at 46% and Delivery accounted for 38%.

In terms of share of wallet, total eGrocery finished the quarter at 13.1%, down from 13.7% last year. Excluding Ship-to-Home (since most conventional grocers don’t offer this service) reveals that the combined Delivery and Pickup share has grown around 40 basis points, accounting for 10.9% of total grocery spending during the first quarter.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!